PM pictures

Author’s note: This article was released to members of the CEF/ETF Income Laboratory on August 12, 2022.

The iShares Floating Rate Bond ETF (BAT:FLOAT) is a diversified floating rate bond index ETF. FLOT focuses on high quality floating rate bonds with short maturities, minimizing credit risk, interest rate risk and overall volatility. FLOT’s holdings are quite safe and the fund has low volatility, but dividends are also quite low, with a forward dividend yield of 2.5%. In my opinion, FLOT is suitable for more conservative investors looking for cash type funds, which are unsuitable for most others.

FLOT – Basics

- Investment Manager: BlackRock

- Forward dividend yield: 2.5%

- Expense ratio: 0.15%

- Total returns 10-year CAGR: 1.2%

FLOAT – Overview

FLOT is a simple floating rate bond index ETF. The fund invests in mostly high quality floating rate bonds denominated in dollars with residual maturities between one month and five years. These three characteristics basically tell us everything we need to know about the fund and its holdings, so let’s take a closer look at them.

Floating rate bonds

A bit of context first.

Most bond and bond funds pay a fixed rate of interest throughout their term, until maturity. When the Federal Reserve raises rates, or when rates move in anticipation of Fed hikes, only the interest rate payments on newly issued bonds change. Older bonds retain their original interest rates.

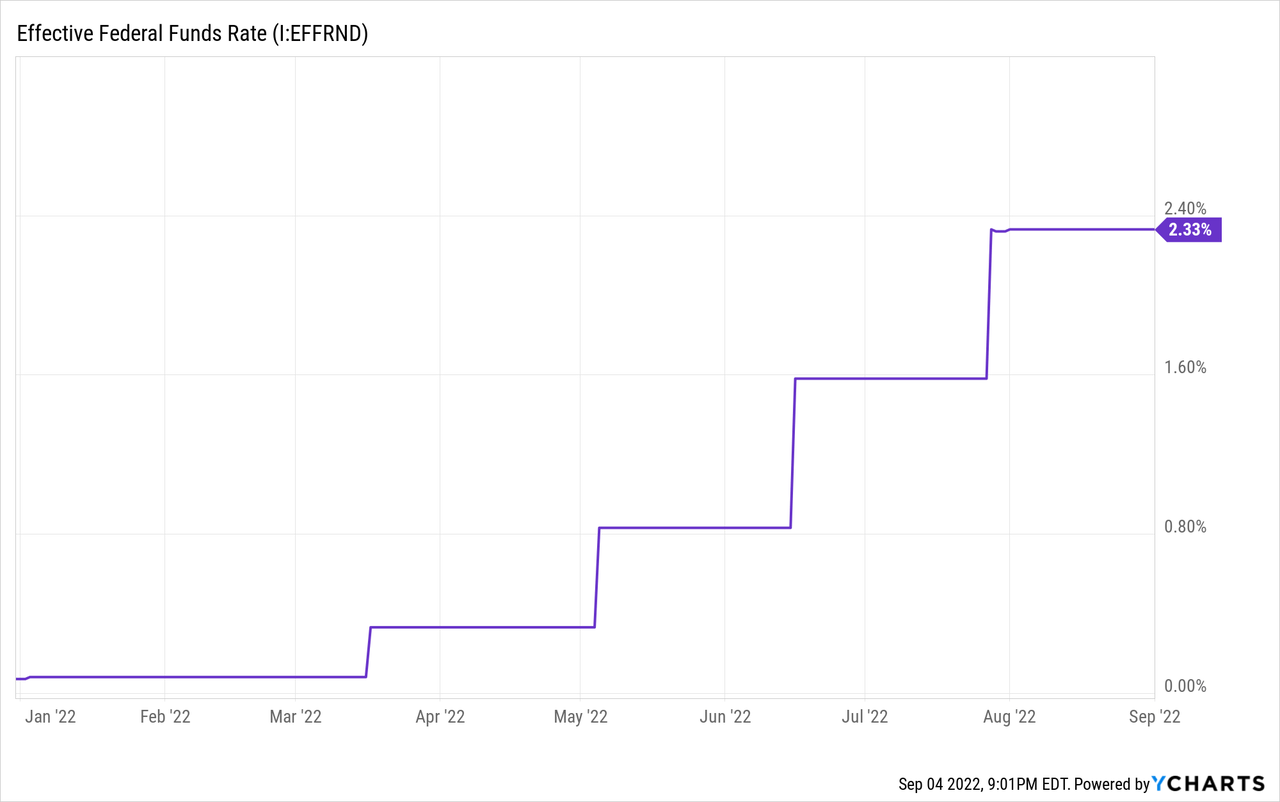

Floating rate bonds, on the other hand, pay a variable interest rate. Interest payments are indexed to a reference rate, usually LIBOR. LIBOR is technically a measure of interbank lending rates but, for all intents and purposes, is equivalent to the Federal Reserve’s target interest rate. The Federal Reserve raises rates, the interest rate on floating rate bonds rises, and vice versa.

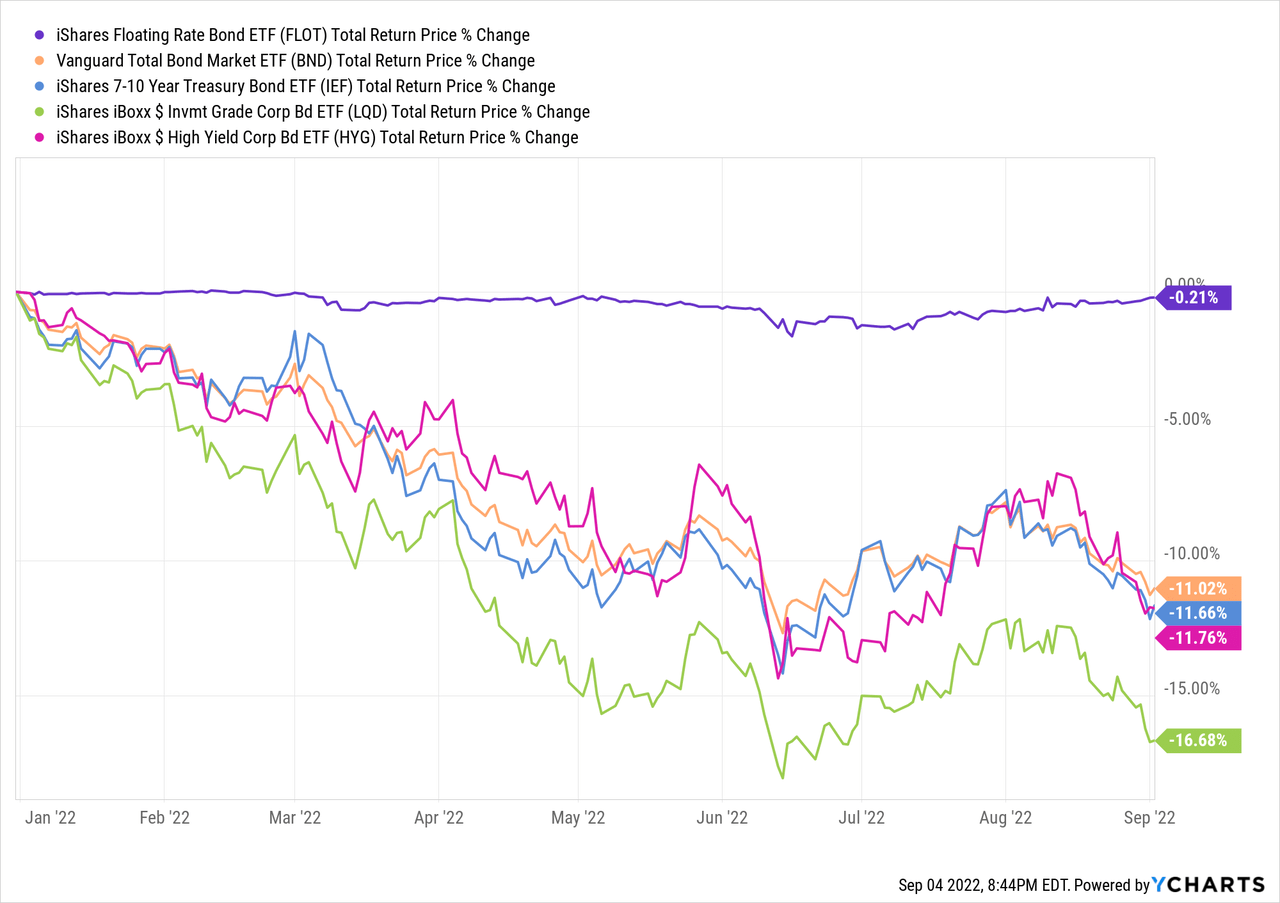

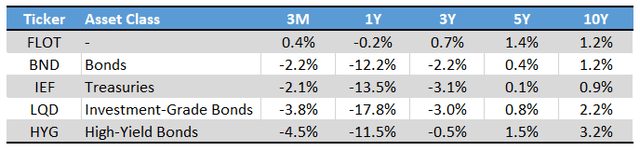

As a result of the above, fixed rate bonds and floating rate bonds behave very differently when interest rates rise. Fixed-rate bonds tend to see their prices plummet when rates rise, as investors sell their old, low-yielding bonds to buy newer, higher-yielding alternatives. Floating rate bonds, on the other hand, see interest rate payments increase when rates rise. Thus, floating rate bond funds tend to outperform comparable fixed rate bond funds when rates rise. FLOT itself has outperformed all relevant fixed rate bond index ETFs year-to-date, as expected.

FLOT’s outperformance during periods of rising interest rates is a significant benefit to the fund and its shareholders, and FLOT’s most important differentiator. Most bond funds will suffer losses when interest rates rise, unlike FLOT. The fund could therefore make sense for investors wishing to avoid said losses / concerned about further interest rate hikes.

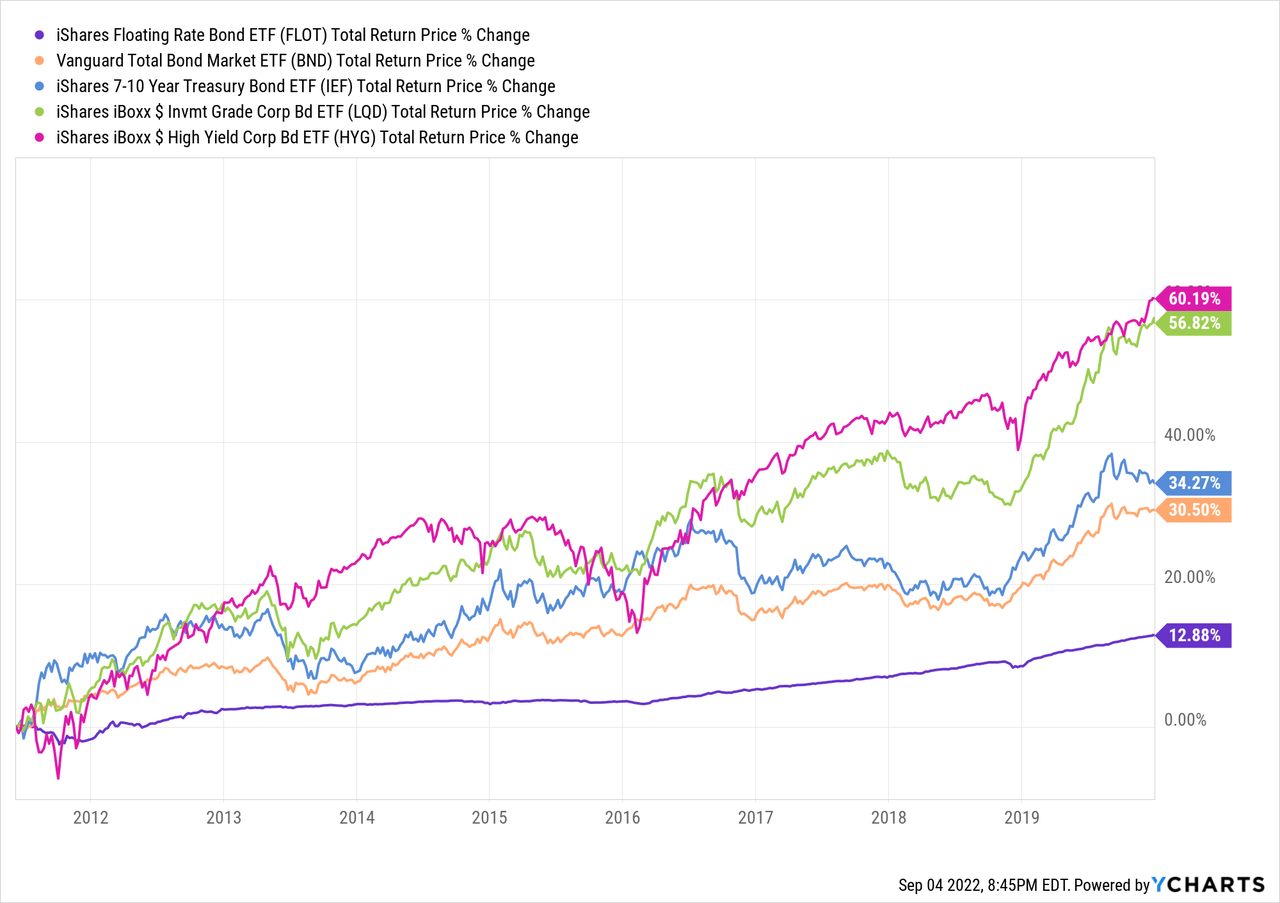

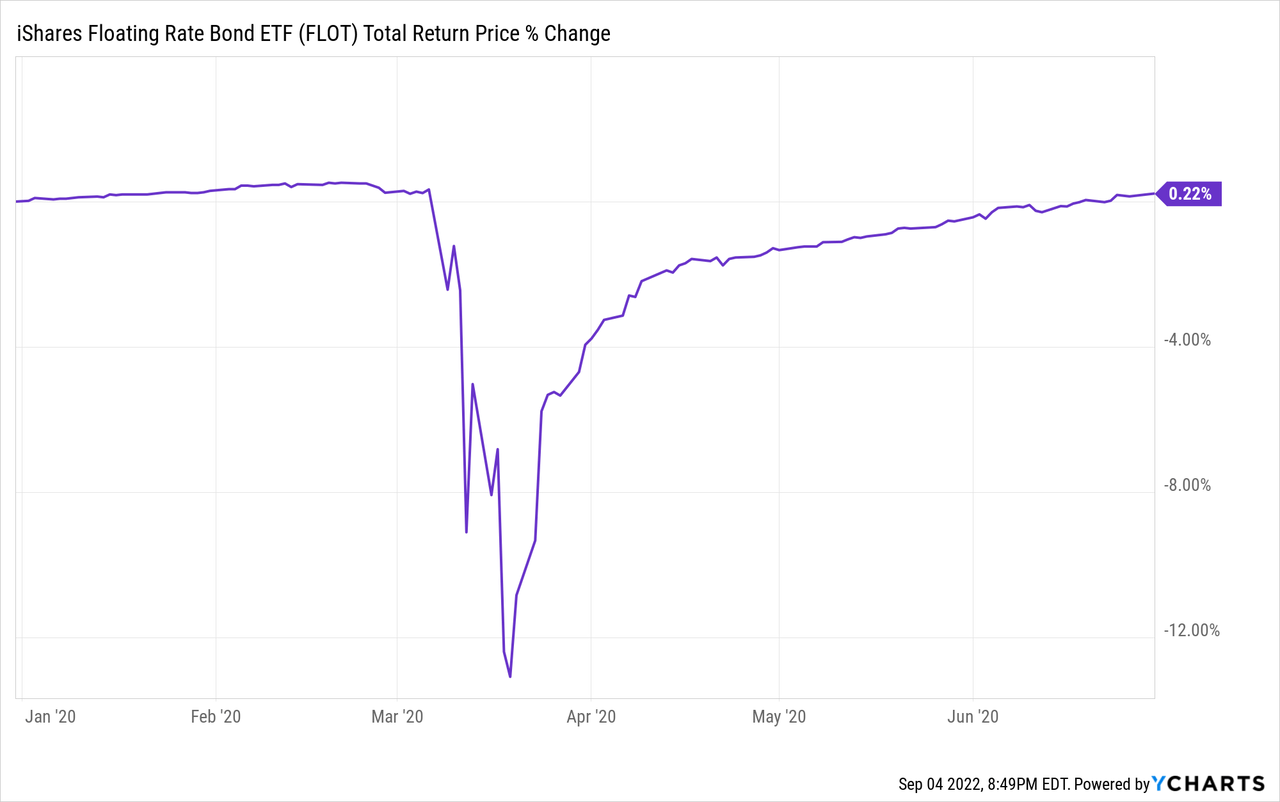

On the other hand, FLOT will generally underperform when the interest rate lessen. Although interest rate cuts seem incredibly unlikely in running economic conditions, conditions can always change and the long term trend is towards ever lower interest rates, due to secular stagnation, demographic plateaus and more efficient and deeper pools of capital. Interest rates have most declined over the past decade, during which FLOT underperformed, as expected. The chart below goes through 2020, in order to focus on periods of declining interest rates, excluding pandemic volatility and recent interest rate hikes.

Bonds of quality

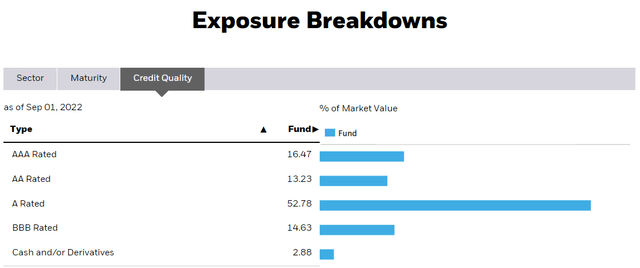

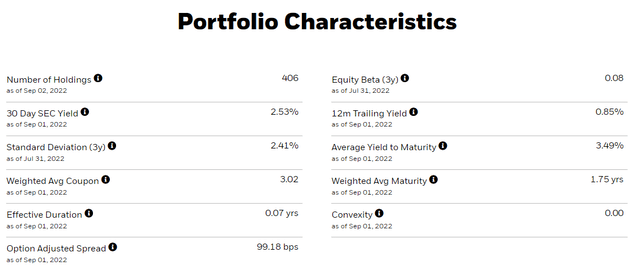

FLOT invests exclusively in high quality bonds with strong credit ratings and issued by companies with strong finances and balance sheets. FLOT’s holdings sport an average credit rating of A, compared to the investment grade average of BBB. This is a solid credit rating, above average for a fund of this type.

FLOW

Strong credit ratings reduce credit risk, default rates and potential losses during downturns. As such, the fund should perform reasonably well during downturns and recessions, as it did in early 2020 at the onset of the coronavirus pandemic. FLOT suffered losses of around 5.0% from peak to trough, but had fully recovered by June. The results were pretty good, all things considered.

Short-term bonds

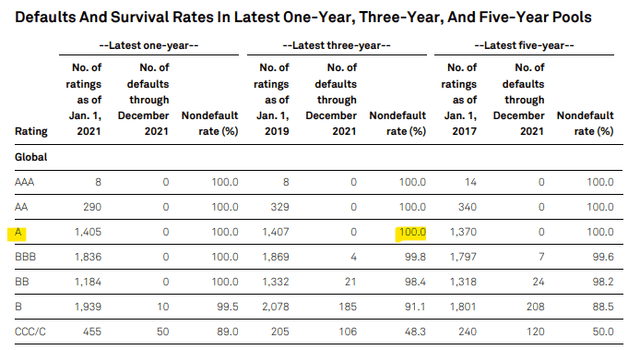

FLOT focuses on short-term bonds, with maturities between one month and five years, and a weighted average maturity of just 1.8 years. Focusing on short-term bonds serves to massively reduce credit risk, as strong companies with strong balance sheets and finances rarely fail in a short period of time. In fact, two-year default rates for investment-grade bonds are effectively zero, and are zero for bonds rated A.

S&P

High quality corporate bonds sometimes suffer from defaults, but rarely within 2 years. A more common phenomenon is that higher quality issuers experience financial difficulties, suffer credit downgrades and go bankrupt a few years later. This process takes time, usually more than two years. FLOT focuses on short-term bonds, avoids these problems, and suffers far fewer defaults than funds focused on higher-quality, long-term corporate bonds.

FLOT’s high-quality, short-term floating rate bonds are safe securities with extremely low credit, interest rate and default risk. As such, and in my opinion, the fund is a relatively safe investment opportunity, particularly suitable for more risk averse investors.

FLOT – Dividend Analysis

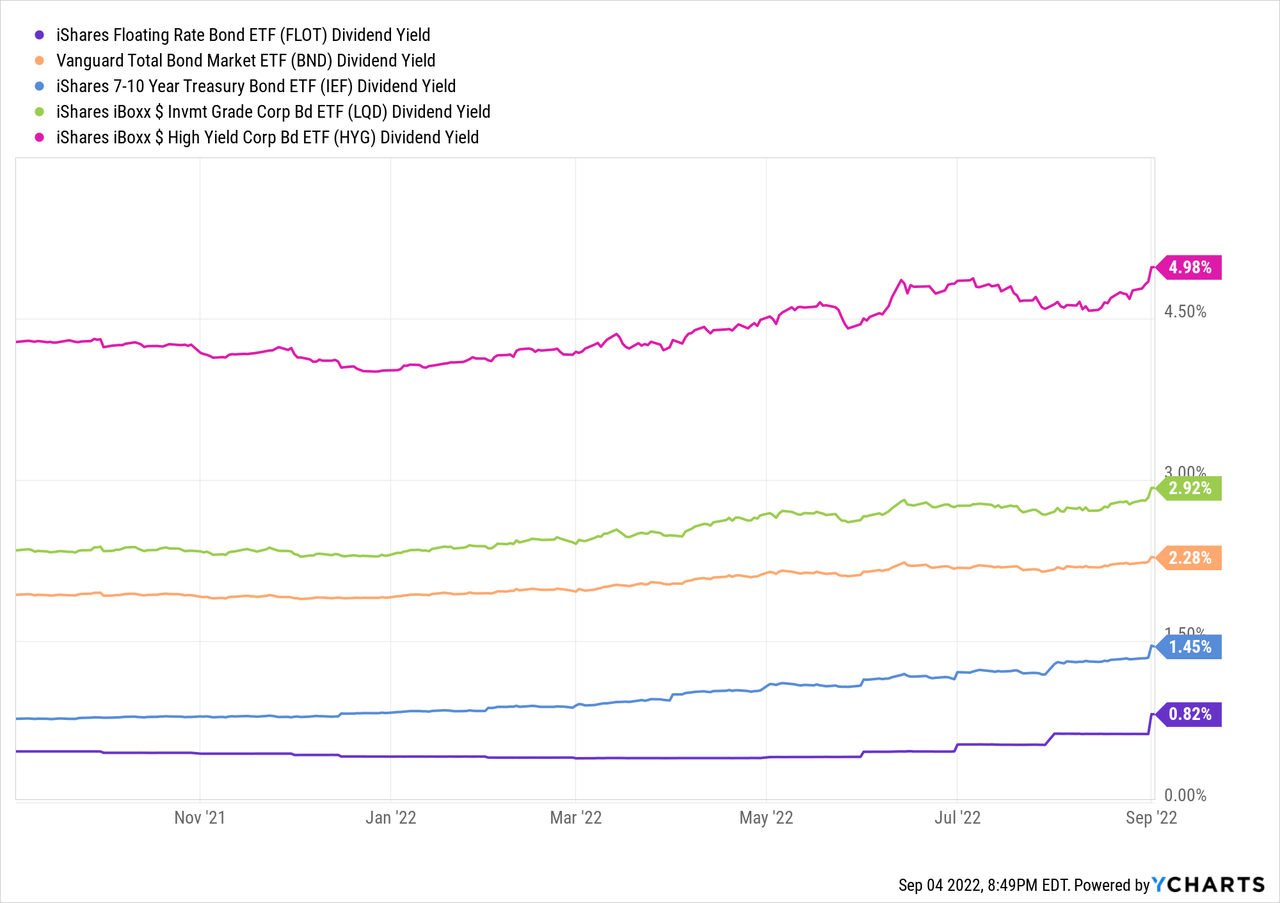

Safe, low-risk stocks and funds tend to have low dividend yields, and this is the case with FLOT. The fund currently has a year-over-year return of 0.82%, an incredibly low number and significantly below its peers.

FLOW

Almost all of the expected dividend growth has also already materialized, the fund’s dividend sixfold YTD. Annualize the last dividend payment, and I arrive at a dividend yield of 2.5%, equivalent to its current SEC yield.

Notwithstanding the above, the fund’s (expected) dividends are low and slightly below average. FLOT is a safe fund, in my opinion, but also a low yielding fund. The combination might make sense for more risk-averse investors and retirees, less so for others.

FLOT – Performance analysis

FLOT’s performance track record is, well, what one would expect from a safe, low-yielding, floating-rate bond. Long-term returns are low, and quite below average, due to the fund’s poor performance. With the fund’s current and expected returns remaining fairly low, investors should expect further long-term underperformance. On the other hand, the fund has clearly outperformed since the beginning of the year, as interest rates have risen. To the extent that interest rates continue to rise, the fund should continue to outperform.

ETF.com – Chart by author

Conclusion

I believe FLOT is a safe fund with low credit, interest and default rate risk. On the other hand, the fund’s yield is quite low, with a forward dividend yield of 2.5%. As such, and in my view, the fund is suitable for more conservative investors looking for cash type funds, which are unsuitable for most others.